Image: InfoLink

InfoLink’s latest ranking, based on data from its energy-storage supply-chain database, shows global energy storage system (ESS) shipments reached 286.35 GWh in the first three quarters of 2025. Shipments exceeded 100 GWh in a single quarter for the first time in Q3, marking a new milestone for the sector.

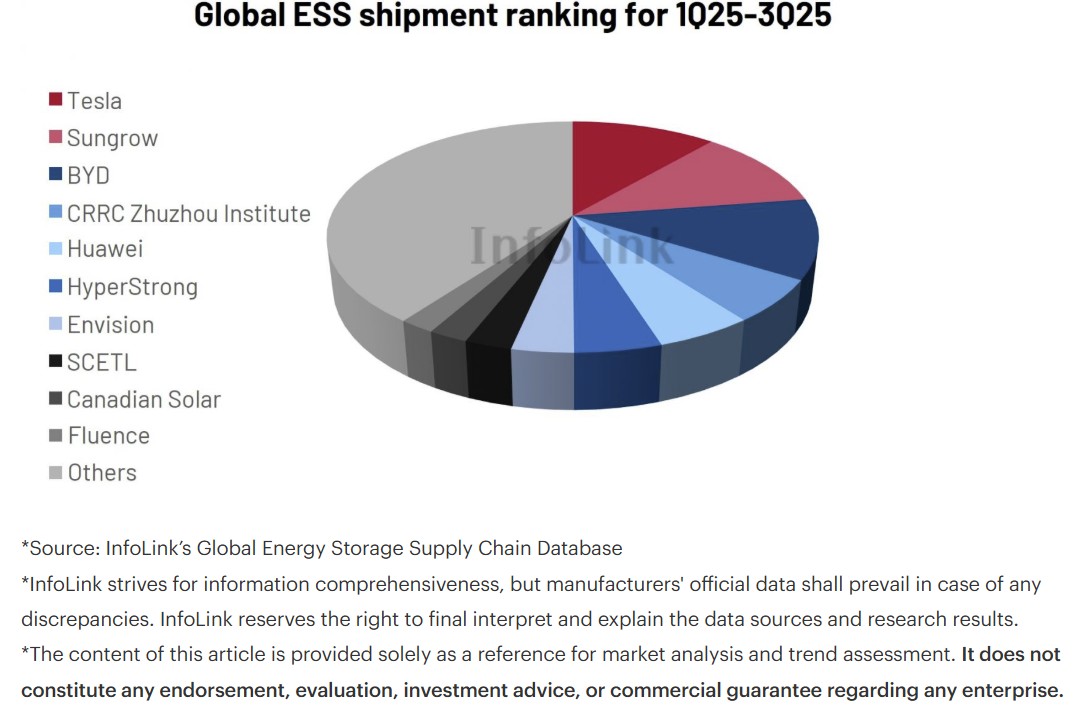

Market concentration remained high, with the top ten suppliers (CR10) accounting for roughly 60% of shipments. InfoLink notes that while a leading cohort has clearly emerged, no single company has yet established dominant control of the market.

Across all ESS system shipments, the top five suppliers were Tesla, Sungrow, BYD, CRRC Zhuzhou Institute, and Huawei. Competition among the top three is described as “fierce,” with their rankings reshuffled again this year—an internal dynamic InfoLink expects to continue through 2026.

A key trend highlighted in the report is the rapid rise of emerging markets. Strong order growth in these regions has enabled major suppliers to expand beyond traditional core markets such as China and the United States. According to InfoLink’s Emerging Market Energy Storage Demand Database, shipments in these newer regions are growing faster than in established markets, making diversified geographic exposure increasingly important for sustaining long-term leadership.

In the residential ESS segment, global shipments reached 26.6 GWh in the first three quarters of 2025, with nearly 10 GWh shipped in Q3 alone. The top five suppliers were Tesla, Huawei, BYD, Pylontech, and Deye. Market concentration increased further, with CR5 rising to 50.9%—about three percentage points higher than the previous quarter—as Tesla and Huawei continued to expand their lead over smaller competitors.

Looking ahead, InfoLink forecasts global ESS shipments will approach 400 GWh in 2025, representing around 60% year-on-year growth, and may rise to about 600 GWh in 2026, maintaining strong momentum. At the same time, the consultancy warns of rising prices in upstream and midstream supply-chain segments. It says system integrators’ ability to manage costs, secure constrained capacity, and protect margins will become a key competitive differentiator as the market enters its next phase of expansion.